Zoom Video Stock: Will History Repeat?

Eric Yuan, founder and chief executive officer of Zoom Video Communications Inc., center, celebrates … [+]

Last year, I called Zoom Video a “pegasus” because the company stood out from the dime-a-dozen unicorns that have come out of Silicon Valley. Zoom has illustrated rare financial strength from its IPO through today due to exceptional product-market fit.

The term unicorn was first used to describe a startup with a valuation of a billion dollars or more. There have been hundreds of unicorns since the term was coined by Ailene Lee of Cowboy Ventures. However, there has been only one tech company on the public markets that has illustrated the financial strength that Zoom Video has in both its top line and bottom line.

Critics will say Zoom required Covid to generate these numbers, yet one look at the S-1 filing immediately disproves this theory. The market is overlooking Zoom’s long history of category-leading growth, which is discussed in detail below.

In the analysis, I also elucidate my thoughts on “exceptional product-market fit” and Zoom’s product strength pre-covid, during covid, and what the company will do to double its TAM in the coming year.

Please also note, per the analysis below, the I/O Fund has closed its position in Bandwidth and allocated more to Zoom. I explain why Bandwidth remains a solid choice yet we see more upside in Zoom due to the company’s sub-Top 20 valuation.

Cloud Software is Not Covid Dependent

During the September 2019 selloff in cloud, which saw 40% to 50% drawdowns in many solid cloud names, I made sure to hammer on my thesis that cloud is a secular trend insulated from geopolitical risks and economic drawdowns. My thesis was proven correct by Covid as cloud software performs well in extreme economic climates because it reduces costs when budgets are constrained, and increases productivity, which is important during times of economic expansion.

This year is very unique for cloud software because many stocks are guiding for less than 40% revenue growth. We are not surprised to see lower valuations following the Q4 earnings reports as the market holds its breath to see how cloud will perform following tough comps from Covid. The Q1 reports are necessary to shed light on what companies will be the leaders coming out of the unusual year of 2020.

There is only one way forward for SMBs and enterprises—adopting cloud IaaS, platforms, and software. Traditional IT is expensive and will only hinder a company from taking advantage of AI and 5G. Competitively it can be very harmful to not transition to cloud right now, as I’ve emphasized in my past reports.

My overarching thesis about cloud software’s resiliency extends to other names, yet this analysis focuses on Zoom Video as it’s one the strongest stocks on the market in terms of its historic top line growth, strong margins, incredible free cash flow and growing profitability. I believe the market is making a mistake by dropping Zoom from the top 20 for cloud software valuations. Zoom is and lay out the reasons below.

Zoom is more than Web Conferencing

The market’s biggest misperception about Zoom is that it’s a web conferencing app. The company is more than two years into developing products and services that broaden its use beyond web conferencing with Zoom Phone launching in January of 2019, yet the market has priced Zoom for only one path (web conferencing). The company has since launched Zoom Rooms, a virtual marketplace Zoom Apps, and OnZoom. The company coined the term hardware-as-a-service because Zoom expects to disrupt nearly every area of telephony.

Last August, I pointed out that Zoom’s hardware-as-a-service products allowed companies to replace legacy systems by consolidating software and hardware for one consistent experience. ServiceNow made headlines last year when they chose Zoom Phone to replace their business phone lines by stating, “Going forward, with the addition of Zoom Phone, we’re getting a head start on an even more robust experience with Zoom— one-touch communication and collaboration features, plus Zoom-connected conference rooms.”

Zoom’s partner program saw significant expansion in 2020. Partner sales bookings increased more than 7x year-over-year. Over 20% of international business bookings in the past quarter were driven by Zoom’s partner ecosystem, and Zoom’s Master Agent business was the fastest growing in history for Master Agents Avant and Intelisys.

Notable partnerships include carriers such as British Telecom, Lumen Technologies, and Orange Business Services. Zoom’s Distributor Partner Program includes Carahsoft Technology Group in the U.S., Nuvias Unified Communications in Europe, eLink Distribution AG in DACH, West Telco in LATAM and EMEA, SYNNEX/Westcon in LATAM, SB C&S in Japan, and FVC in the Middle East and Africa.

Master agents AVANT Communications and Intelisys, a ScanSource company, both reached $1 million in monthly recurring revenue (MRR) prior to the one-year anniversary of their partnerships with Zoom. Zoom also added six new Master Agent partners: AppSmart, Bridgepointe, eLink Distribution, PlanetOne, Sandler Partners, and Telecom Consulting Group (TCG).

Last year, Zoom saw growth of use cases in telemedicine, virtual events, and health and fitness after revamping its partnership program for independent software developers. The company supports more than 200 partners through its open API and SDK and expects to see further growth as new industries and markets are developed on top of Zoom.

Zoom also recently announced a multi-year partnership with Formula One, following a successful collaboration in 2020 on the Virtual Paddock Club, which offers VIP sports experiences. As part of the expanded partnership agreement, Zoom is working with Formula 1 to deliver unified communications and new business and hospitality experiences for on-site and virtual guests, including live updates from “legends of the paddock” and Paddock Club Business Lounges set up in Zoom Rooms.

Forward CAGR & Product-Market Fit

The analyst estimates for Zoom are 29.8% CAGR over the next three years through fiscal 2024. This makes little sense as the company has had a net retention rate of 130% over eleven consecutive quarters. This means analysts are essentially guiding for an increase in churn/downgrades and these projections assume Zoom will not add any new customers.

The analyst estimates for Zoom are 29.8% CAGR over the next three years through fiscal 2024.

As stated, management from cloud software companies are not giving analysts much for forward guidance as it’s better to play this transitional period safe. Regardless, the projections don’t match Zoom’s incredibly strong track record.

First, there is no other cloud software stock that has made the leap from enterprise to consumer. Zoom was the top app by number of customers and unique active users this past year. Yet, it is also the preferred enterprise video conferencing app and ranked among the most popular workplace apps overall, according to Okta’s 2021 Business Network Report.

We see further evidence of Zoom’s customer approval across both consumer and enterprise as the security concerns last year were quickly forgiven as the management moved quickly to respond. In Q4, Zoom Phone was the fastest growing product line quarter-over-quarter. During the most recent earnings call, Zoom announced expansions into Zoom Phone by Zoom Meetings customers Equinox, Universal Music Group, and University of Southern California. The company expects strong growth for Zoom Phone going forward with a strategy of selling into the existing install base.

For product-market fit, you need the top line to grow rapidly and for the bottom line to strengthen. This is not the only indication but it simplifies the many variables. Before I go over the recent financials, I want to emphasize that Zoom was already outperforming its category per the S-1 filing that I covered in April of 2019.

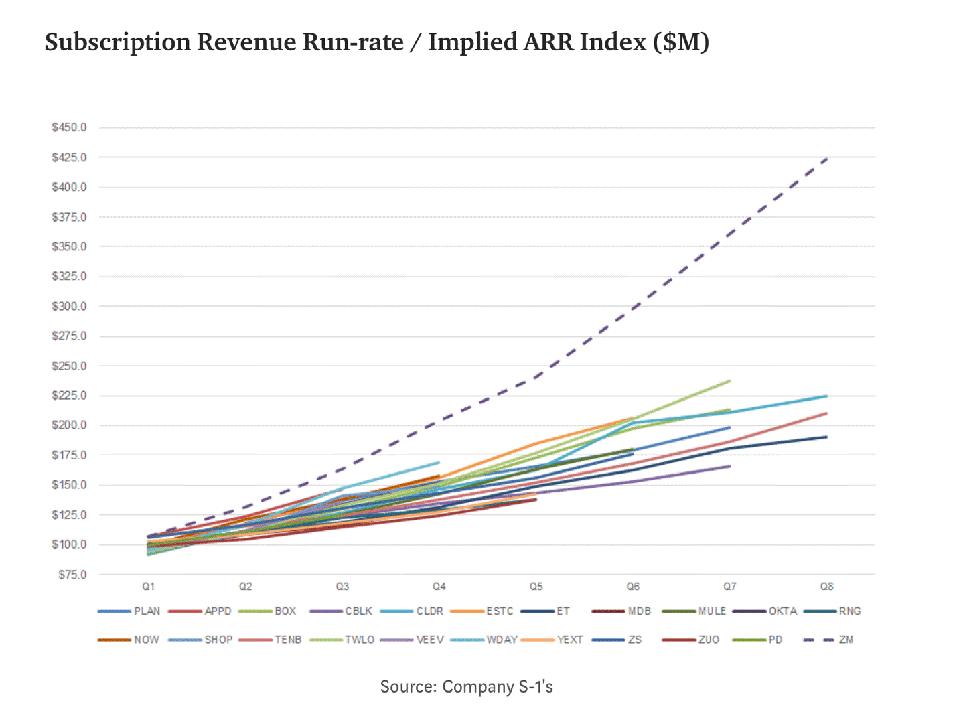

The chart below provided by Alex Clayton of Spark Capital shows how Zoom compares to other cloud software companies that had a subscription revenue run-rate of $100M in their disclosure period with the graph indexed to the quarter where they crossed $100M.

Not only was Zoom the fastest growing cloud software IPO from $100 million onward in terms of run … [+]

Source: Alex Clayton, Spark Capital

Not only was Zoom the fastest growing cloud software IPO from $100 million onward in terms of run rate but also grew 108% in their last quarter YoY compared to a median of 38% in 2018 for the companies pictured above. Zoom was also the most efficient in terms of customer acquisition cost, with a median payback period of 9 months compared to the median of 30 months.

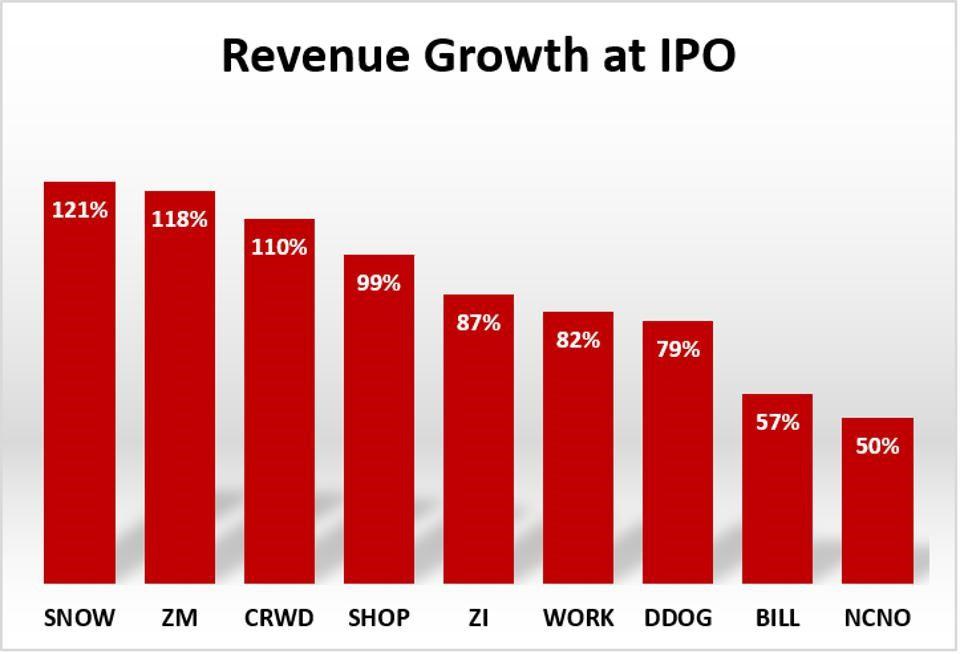

Below is how Zoom stacked up to other popular cloud software stocks at its IPO:

How Zoom stacked up to other popular cloud software stocks at its IPO

There’s a catch to the graph illustrated above — Snowflake was only 6 years post-launch while Zoom was 8 years post-launch. Therefore, when we adjust growth rates for age of company, we see Zoom is the #1 company in terms of financial strength in cloud software:

We see Zoom is the #1 company in terms of financial strength in cloud software.

There’s more … Zoom was profitable at the time of IPO while the majority of cloud software companies are not profitable many years after their IPO. Not only is Zoom the strongest IPO in cloud’s history but it was also profitable. Not one other company was profitable at IPO … and only Shopify is profitable now from the list although this occurred many years after Zoom if we adjust for age of company.

Hopefully, this helps the critics see that Zoom has always been best in its class – and cloud software is not an easy category to lead with top performers such as Crowdstrike, Snowflake, Shopify and Slack (a very sticky product) coming from this category.

Doubling TAM

Founded in 2011, Zoom previously described itself as a leader in modern enterprise video communications. The CEO states that Zoom is enabling greater effectiveness in human-to-human interactions over a distance with use cases that are not possible with legacy systems. The key words here are “not possible with legacy systems.”

Zoom’s ongoing goal will be to disrupt all legacy systems with cloud-native communications – and this means every possible method of communication that is not currently done on the cloud and/or is currently on the cloud but is too cumbersome of a process due to walled gardens.

According to Gartner, by 2022, 65% of meeting solutions users will take advantage of SIP/VoIP-based audio-conferencing tools. This is up from 20% in 2017, while 40% of meetings will be facilitated by virtual concierges and advanced analytics. Here we see Gartner had already predicted audio-conferencing to grow substantially prior to Covid.

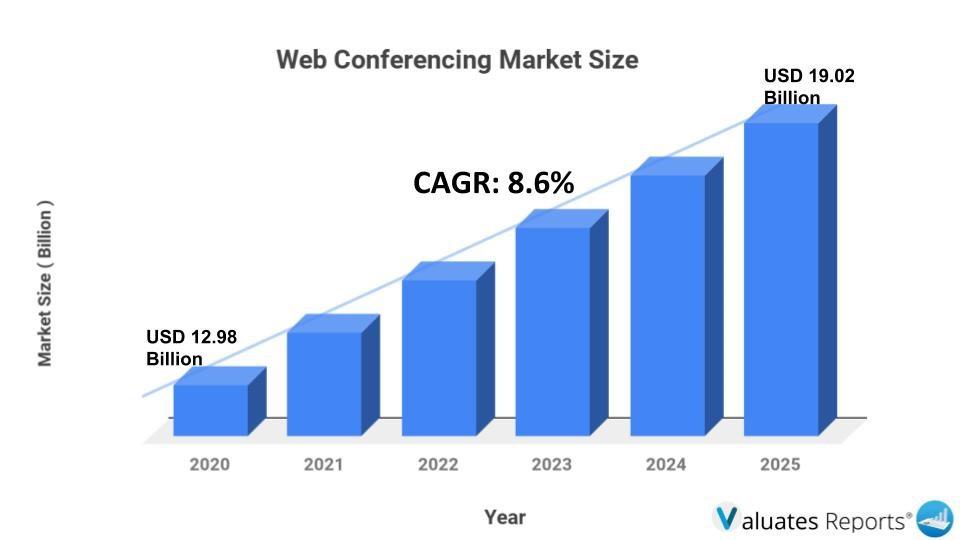

The global web conferencing market is expected to grow from $12.58B in 2020 to $19.02B by 2025, at a CAGR of 8.6%, according to Valuates, which offers market research reports.

The global web conferencing market is expected to grow from $12.58B in 2020 to $19.02B by 2025, at a … [+]

The exact size for the video communications market varies considerably depending on the source. This is because the market is very new. According to research from Markets and Markets, the video communications market is expected to grow an average of 8% per year to nearly $20 billion by 2023, with another report expecting that the industry will register a CAGR of 9.2% from 2018 to 2025. However, IDC pegs Zoom’s future addressable market much higher at $43 billion, as cited in a previous Zoom earnings call.

If we go with the more modest addressable market size of $20 billion, then Zoom Phone will double TAM as telephony is forecast to grow to $23 billion by 2024, per the Q4 fiscal 2021 report. While doubling TAM, Zoom Phone was the company’s fastest-growing product line quarter-over-quarter, according to the report, and executives expect to see strong growth in FY2022.

Some analysts claim the domestic market is close to saturation, and Zoom will have to look for more opportunities in overseas markets. This is unlikely as communications is both account based and usage based, not to mention hybrid work-from-home is the consensus among surveys of executives with only 29% stating the office will return to five days in the office per week.

Zoom sees international expansion as a major opportunity. In the first-quarter fiscal 2020, APAC and EMEA revenue grew a combined 127% year-over-year. As such, Zoom plans to add local sales support in further select international markets over time and also use strategic partners and resellers to sell in international markets.

Revenue from APAC and EMEA collectively represented about 20% of Zoom’s revenue for the quarter and management noted that it could be the beginning of a sizable opportunity to bring the Zoom platform to other regions.

Why Zoom Went Viral and Will Again …

The agnosticism of Zoom compared to Google and Microsoft means the company has the opposite goal of big tech: rather than lock users into a walled garden, Zoom created a flawless and viral mechanism where users can share web and audio-conferencing links without needing to login. Zoom exploited big tech’s weakness – the walled garden – which requires logins and a cumbersome user work flow.

Many critics think the catalyst for the virality was Covid, yet my premium site had stated this mechanism was a viral feature many months prior to the pandemic. “Viral mechanic” means the spread of growth across users as a built-in mechanism to the product. The first Zoom user in an office naturally evangelizes the product by inviting more people to a conference with a simple link. The users who are invited do not need to sign up for Zoom, and the experience is much better than other conferencing solutions that require many steps to join a conference and are not in HD.

The best growth in tech products occurs when the product multiplies across users exponentially. This is why social media reported incredible growth – one user invites many users to the platform with a simple link. Zoom is an example of the “sum of its parts is greater than the whole.” Its success is based off many micro improvements to video conferencing that adds up to a serious advantage over the competitors.

Cisco was the main competitor that Zoom disrupted as CEO Eric Yuan was a former engineer at WebEx before it was acquired by Cisco. Zoom has a “bottoms-up” viral customer base, which means junior employees evangelize the service at the company. These are often some of the most loyal customers. For instance, 55% of $100,000 or higher revenue customers were started with a single employee’s free trial. This is an important insight to the traction of the product.

Zoom’s virality with web conferencing is important because I expect the same team (and for the same reasons) to create a frictionless and viral method to replace all forms of legacy communications.

Zoom’s Current Quarter & Forward Growth

In most recent quarter, Zoom reported Q4 revenue of $882.5M, representing growth of 369% YoY, beating expectations by $71.54M. Non-GAAP EPS of $1.22 beat by $0.43 and GAAP EPS of $0.87 beat by $0.39.

GAAP income from operations was $256.1M, up 2327% year-over-year. Non-GAAP income from operations was $360.9M, up 839% YoY.

For the full year, total revenue was $2,651.4 million, up 326% year-over-year. GAAP income from operations for the fiscal year was $659.8M, compared to GAAP income from operations of $12.7 million for fiscal year 2020. GAAP operating margin was 24.9% and adjusted operating margin was 37.1%.

Please note, when you see this level of bottom-line growth, it means Zoom is spreading organically and not needing to pay for its growth. This is extremely rare in Silicon Valley and other tech startup hotbeds, as growth marketing is a tactic used to grow the top line at the expense of the bottom line.

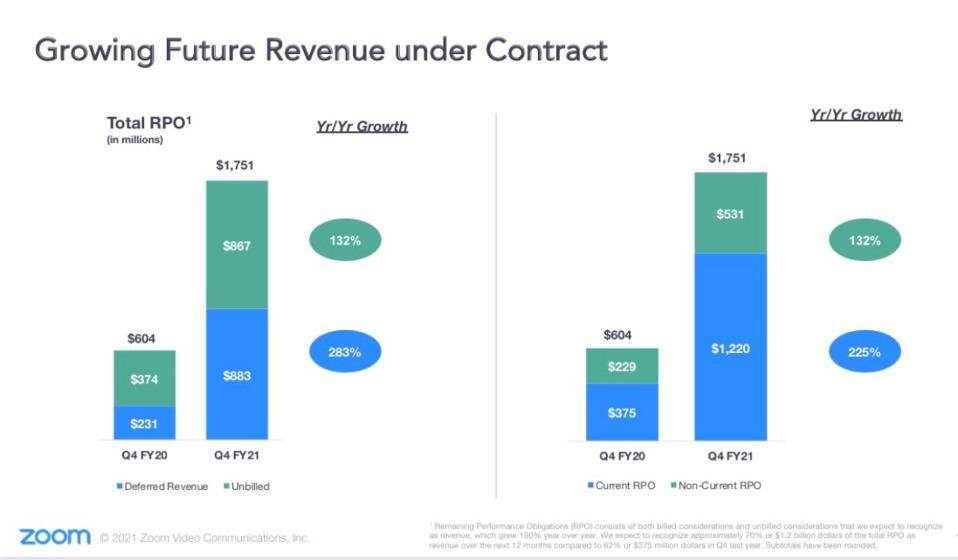

Remaining performance obligation was up 189% year-over-year from $604 million to $1.75 billion with the company expecting to realize 70% of this amount in the upcoming year. This means before the fiscal year even began, the company will have already have $1.22 billion of revenue in the pipeline of the $3.7 billion projected for the year.

Remaining performance obligation was up 189% year-over-year from $604 million to $1.75 billion with … [+]

Non-GAAP net income for the fiscal year was $995.7M, after adjusting for stock-based compensation expense and related payroll taxes, expenses related to charitable donation of common stock, acquisition-related expenses, and undistributed earnings attributable to participating securities. Non-GAAP net income per share was $3.34. Non-GAAP net income was $101.3 million, or $0.35 per share.

Net cash provided by operating activities was $1,471.2M for the fiscal year, compared to $151.9M last year. Free cash flow, which is net cash provided by operating activities less purchases of property and equipment, was $1,391.2 million, compared to $113.8 million last year.

Zoom provided the following guidance for fiscal year 2022:

· Total revenue for Q1 is expected to be between $900.0M and $905.0M vs $835.35M consensus

· Non-GAAP income from operations is expected to be between $295.0M and $300.0M.

· Non-GAAP diluted EPS is expected to be $0.96 at the midpoint versus $0.70 consensus

For the full year, total revenue is expected to be $3.770B versus $3.5 consensus, representing growth of approximately 30% YoY, and non-GAAP income from operations is expected to be between $1.125B and $1.145B.

Full fiscal year non-GAAP diluted EPS is expected to be between $3.59 and $3.65 versus $2.96 consensus, with approximately 311 million non-GAAP weighted average shares outstanding.

In the last three months, 20 analysts set 12-month price targets for Zoom, according to data from E*Trade. The average price target was $472.41, with a low of $360 and a high of $610 representing 98% upside from the current price.

Finally, it’s worth mentioning that the Zoom app is still #1 on the business charts in the App Store.

At the end of first-quarter fiscal 2020, the company had roughly 58,500 customers (with more than 10 employees), up 86% year over year. Zoom has a strong partner base that includes companies such as Salesforce, and these partnerships will be instrumental in future growth. Zoom ended the last fiscal year with more than 467,000 customers with more than 10 employees, up approx. 470% from the same quarter last fiscal year, according to the report.

Bandwidth

One reason we closed our position in Bandwidth is that we feel work-from-home should have been a bigger catalyst for Bandwidth, with major customers including Zoom, Google, Microsoft enterprise, Skype, RingCentral and Square. If there was ever a year that a Tier 1 provider should have seen rapid growth with these customers, last year would have been the year. Instead, for the full year 2020 we see Bandwidth with total revenue of $343.1M, up 48% YoY, versus Square (for example) which reported total net revenue of $9.50B, up 101% YoY for the full year 2020.

Bandwidth is a communications platform-as-a-service (CPaaS) company that offers voice, messaging and 911 APIs built on the company’s Tier 1 network. Although Bandwidth competes in a similar area as Twilio and Messagebird, the company is distinguished by owning its network and by offering competitive pricing and a stripped-down version of voice and SMS.

The company works with the very largest VoIP and video/audio conferencing companies including Google, Microsoft, Skype, Zoom and Ring Central. The work-from-home trend has benefited Bandwidth’s customers. There is a potential for another catalyst, which is the expansion into Europe. This is important as Europe in particular has proven to be a major market for VoIP due to various country codes in close proximity.

Bandwidth is overshadowed by competitors, including Twilio and Messagebird. Five9 is also in the adjacent space of the cloud contact center (top of the stack as a complete solution)

The difference between these companies is important to understand. Twilio enables communications for mobile applications, such as voice or text. When you text or make a call inside of a mobile application, you are likely using Twilio’s APIs. The company works with over 1,000 mobile carriers in over 150 countries for voice and text/SMS services. The features that come pre-packaged with Twilio are ideal for companies who want to cut down on development time, such as startups or pureplay apps. Examples include customer service calls on Zendesk and messaging home owners inside the AirBnB app.

However, large companies in the video and phone conferencing space (including business apps), with a primary focus on communications, are unlikely to incorporate an expensive third-party for out-of-the box development. As a network carrier, Bandwidth undercuts Twilio on pricing with cheaper outgoing and incoming calls plus free incoming SMS. This option is entirely focused on voice and SMS while its customers develop any additional features in-house. Twilio costs $1 for a dedicated number while Bandwidth costs $0.35 per dedicated number. This is why Bandwidth is the network provider for Google, Microsoft enterprise apps and Skype, and also Zoom.

On the flip side, Bandwidth makes a fraction of a penny for every call or message that is sent over the Tier 1 network. Therefore, Bandwidth’s revenue is not up to par with Twilio’s at about $280 million compared to $1.5 billion.

The issue may be that what Bandwidth offers is more commoditized between the various telephone networks and also cellular. Therefore, the better investment may be in the full product stack, like what Zoom offers.

More on Bandwidth’s Financials …

Excluding the acquisition of Voxbone, which closed last quarter, Bandwidth’s standalone CPaaS Q4 YoY revenue growth was 53%. Tailwinds include political messaging and factors related to Covid-19. Political messaging and Covid-related usage contributed 19 points to the company’s Q4 YoY growth rate, according to the report.

Where dedicated, daily user behavior within enterprises around VoIP and cloud native conferencing apps may have been many years out, covid-19 has sped this up. The addressable market growth was estimated to be about $1.7 billion in 2017 to $6.7 billion in 2022 for this market. Yet, we think one issue with Bandwidth having lagging growth for this category is there was too much competition for Bandwidth to increase its market share.

The recent quarter was impressive with 82.3% revenue growth yet the previous quarters were in the 30-40% range. Despite these normal comps, the company is guiding for 58% growth year-over-year for the March quarter.

Within total revenue, CPaaS revenue was $98.1M, up 84% YoY. Other revenue contributed the remaining $14.9 million for the quarter. Other revenue was $8.6 million in the same period last year. Total, CPaaS, and Other Revenue include $17.5M, $16.6M and $0.9M respectively from Voxbone starting on Nov. 1, 2020, the date of the acquisition.

Adjusted gross profit was $55.8M, compared to $31.1M for Q4 2019. Adjusted gross margin was 49% compared to 50% for Q4 2019.

Adjusted net income was $3.5M, or $0.13 per share, based on 27.2 million weighted average diluted shares outstanding. This compares to a Non-GAAP net loss of $(0.5)M, or $(0.02) per share, based on 23.5 million weighted average shares outstanding for the fourth quarter of 2019. Adjusted EBITDA was $8.3M, compared to $1.2M in Q4 2019.

Total revenue for the full year of 2020 was $343.1M, up 48% year-over-year. Gross profit for the full year 2020 was $157.9M, compared to $107.6 million in 2019. Adjusted gross profit for the full year of 2020 was $169.1M, compared to $114.4M in 2019. Adjusted gross margin was 49% for the full year of 2020 and 2019.

In the last three months, five ranked analysts set 12-month price targets for Bandwidth, according to date from E*Trade. The average price target is $210, with a low of $200 and a high of $227 for an upside of approx. 95%.

On the bullish side, Canaccord Genuity raised its price target from $175 to $225 after Bandwidth’s acquisition of Voxbone, stating the purchase: “accelerates Bandwidth’s international expansion plans and creates a stronger position in the global $18B CPaaS market.”

JMP raised BAND from $180 to $206, favoring the deal “because it accelerates Bandwidth’s international expansion in a way that is accretive to its non-GAAP gross margins and non-GAAP net income.”

Conclusion:

Inertia matters with tech growth. The companies that grow rapidly tend to continue to do well long-term. Zoom has been dropped out of the top 20 in terms of valuation for the cloud software category and is now cheaper than before the pandemic, which led to the best earnings reports of any company in Wall Street history. Due to the low valuation and the company having plans to double its TAM quickly, among other reasons, we have closed Bandwidth in favor of a larger position in Zoom.

Disclosure: Beth Kindig owns shares of Zoom Video. The information expressed herein are opinions and not financial advice.