These 6 Words From Micron’s CEO Could Spell Big Returns for Investors

Micron Technology (NASDAQ: MU) continues to post strong operating results. In the fiscal second quarter, revenue and earnings per share came in above management’s guidance. The company is leading the memory solutions industry in driving down costs, growing profits, and delivering new technologies.

In the company’s recent March earnings report, CEO Sanjay Mehrotra promised that Micron had big things ahead, saying that “our product portfolio momentum is accelerating.” Those six words from the CEO suggest Micron is just getting started. Let’s take a look at what’s fueling the company’s momentum and why the stock might be the best bargain in tech.

Image source: Getty Images.

Micron’s incredibly cheap stock

Shares of Micron have returned 76% over the last three years but are down 19% year to date. Based on the consensus earnings estimate for Micron’s fiscal 2022, the stock trades at a cheap price-to-earnings (P/E) ratio of just eight. Micron is a leading memory chip provider that is positioned to see strong growth over the next decade, especially cloud-based computing applications, the stock offers great value.

Investors are discounting the stock because selling prices for memory and storage products are historically subject to price volatility. A sudden price drop would obviously cause uncertainty for Micron’s near-term revenue growth and profitability. Sales of dynamic random access memory (DRAM) make up three-quarters of Micron’s revenue, but it’s a highly competitive market.

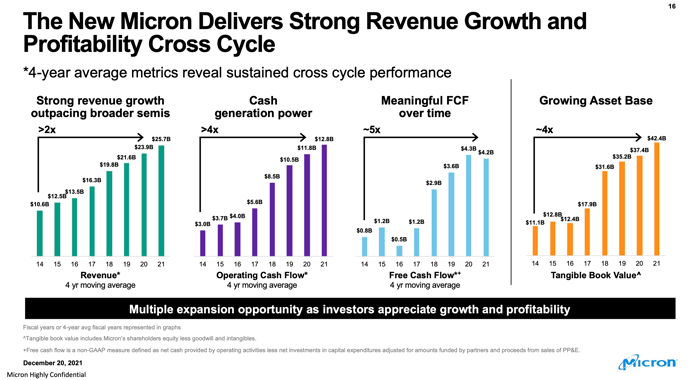

That competition has historically driven swings in selling prices and lumpy operating results. Still, Micron has reported steady growth in revenue and free cash flow (FCF) when looking at its performance on a four-year moving average. Using a trailing four-year average, Micron more than doubled its revenue from fiscal 2014 to fiscal 2021 to reach over $25 billion. FCF grew even faster, rising from less than $1 billion to over $4 billion.

Image source: Micron Technology.

Micron’s growing product portfolio

Micron recently launched its new 7450 solid-state drives for data centers using what the company calls 176-layer non-volatile storage (NAND) technology. NAND is a type of flash memory used in solid-state drives. This fills a huge need for the surge in cloud services that is driving up demand for additional data processing and storage, and the faster data retrieval speed of flash memory is what companies are really looking for these days.

Also, Micron sees a surge in momentum heading into 2023 and anticipates that more data centers will transition to Micron’s faster DDR5 memory, as well as more consumer PCs featuring DDR5 memory. These products are based on Micron’s new 1-alpha DRAM technology, which feature improved performance to feed data-hungry applications like mobile devices, electric vehicles, and data centers.

In the last quarter, Micron’s 1z and 1-alpha DRAM represented most of the company’s DRAM bit shipments. On the other side, Micron’s 176-layer NAND comprised most of its NAND bit shipments. These technologies contain higher bit density and offer impressive performance, two factors that result in lower production costs and, thus, higher margins.

A strong financial profile

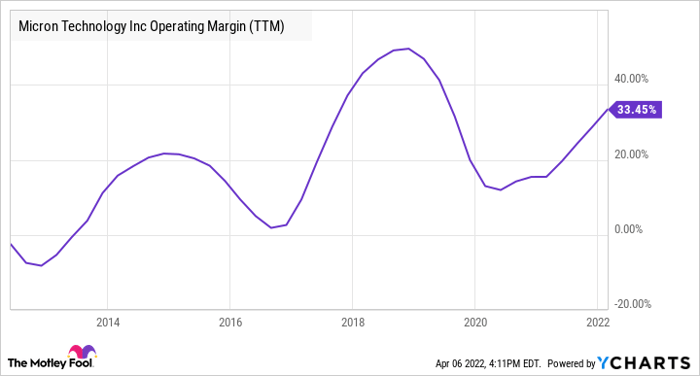

Micron originally announced its first shipment of DRAM based on 1-alpha technology at the beginning of 2021. Since then, Micron’s operating margin has improved from 20.2% in the year-ago quarter to 35.3% in the fiscal second quarter of 2022.

Prices for the faster DDR5 memory are pacing ahead of those for the previous DDR4 generation, which is good news for Micron’s margins. The reduced manufacturing cost of these new DRAM and NAND products helped Micron post higher gross margins in the fiscal second quarter, up to 47.8%, an improvement of 80 basis points quarter over quarter.

Micron’s innovation and efforts to lower manufacturing costs have gradually firmed up its operating margin over the last 10 years. Even better news for investors? The company’s expanding suite of products and improving financial background suggests that the company is not done growing.

MU Operating Margin (TTM) data by YCharts

Supply chain problems and inflationary costs could present some challenges in the near term, but most importantly, management expects the company’s cost reductions to outpace its competitors’ this year. That positions Micron for industry-leading business performance, which should lend this low-P/E stock a higher valuation.

Growth expectations

Micron sees healthy demand in data centers, the adoption of 5G smartphones, and continued strength in the automotive and industrial markets driving another record year. Analysts currently expect Micron to post revenue and earnings growth of 21% and 58%, respectively. Next year, analysts expect revenue to advance another 20%, with earnings rising 32%. In a market where it’s difficult to find genuinely undervalued stocks, Micron looks like a good bet in 2022.

10 stocks we like better than Micron Technology

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now… and Micron Technology wasn’t one of them! That’s right — they think these 10 stocks are even better buys.

*Stock Advisor returns as of March 3, 2022

John Ballard has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.